(HedgeCo.Net) In reporting fourth-quarter and full-year 2025 results on January 29, 2026, Blackstone highlighted $71.5 billion of inflows in the quarter (its highest in more than three years) and $239.4 billion for the year, pushing total AUM to $1.2749 trillion. The numbers confirm that, while investors still debate the durability of private markets in a “higher-for-longer” world, capital is continuing to consolidate with the biggest platforms—especially those that can deploy at scale into secular-growth infrastructure and generate realizations as exit markets reopen.

The headline scorecard: fundraising momentum, earnings resilience, and $1.3 trillion scale:

Blackstone’s release framed Q4 as the capstone to a record year. CEO Stephen Schwarzman said the firm “delivered again” for limited partners, pointing directly to the quarter’s inflow surge and the firm’s focus on “massive scale” investing in digital and energy infrastructure. That emphasis matters: it positions Blackstone not simply as a diversified alternatives manager, but as an institutional conduit for one of the largest capital buildouts of this decade.

Financially, Blackstone reported:

- Fee Related Earnings (FRE): $1.5 billion in Q4 ($1.25/share); $5.7 billion for FY 2025 ($4.67/share)

- Distributable Earnings (DE): $2.2 billion in Q4 ($1.75/share); $7.1 billion for FY 2025 ($5.57/share)

- Total AUM: $1.2749 trillion; Fee-Earning AUM: $921.7 billion; Perpetual Capital AUM: $523.6 billion

- Deployment: $42.2 billion in Q4; $138.2 billion for the year

- Realizations: $46.1 billion in Q4; $125.6 billion for the year

For shareholders, Blackstone declared a quarterly dividend of $1.49 per share (payable February 17, 2026, to holders of record February 9, 2026) and said it would distribute roughly $2.0 billion to shareholders related to Q4and $6.2 billion for the year through dividends and repurchases.

In an environment where public markets have whipsawed around rate expectations and recession probabilities, Blackstone’s message was clear: management fees and fee-related earnings remain durable, while realizations and performance revenues can expand meaningfully when M&A and IPO windows reopen.

Why Q4 mattered: realizations, “escape velocity” in deals, and the return of the exit market

A key driver in Blackstone’s quarter was the improvement in activity across exits and monetizations. Reuters described Blackstone as riding “escape velocity” in dealmaking to beat profit expectations, noting $957 million from asset sales in Q4 (up 59% year over year) alongside broader signs that the M&A market is reviving.

That’s an important tell for the entire alternatives complex: realizations don’t just create performance income—they recycle capital, improve DPI narratives, and unlock the next fundraising cycle. In private equity especially, the last few years were defined by the “exit drought,” with sponsors sitting on mature assets while buyers demanded discounts. Blackstone’s results suggest that logjam is easing, even if unevenly.

The firm’s own reported $46.1 billion of realizations in Q4 reinforces the point that liquidity is returning to private markets in a more material way. When the exit environment improves, the flywheel engages: realizations strengthen fund performance optics, LPs re-underwrite allocations, and the largest platforms capture incremental share.

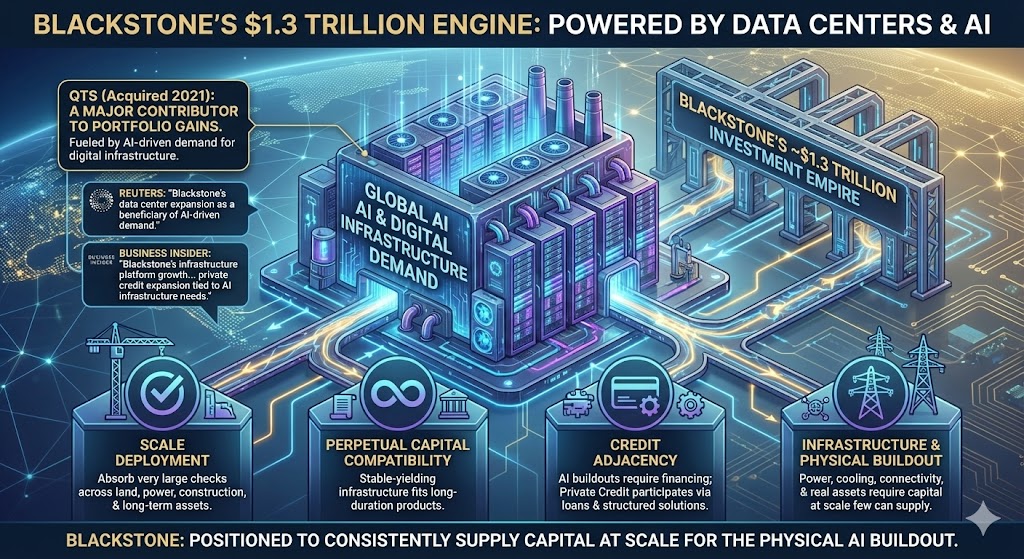

The real strategic headline: AI is turning data centers into the new “core infrastructure”

If you want the simplest narrative thread across Blackstone’s 2025 results, it’s this: the firm has become one of the biggest “picks-and-shovels” financiers of the AI era. That shows up most visibly in data centers.

Business Insider described data centers as powering Blackstone’s roughly $1.3 trillion investment empire, citing QTS (acquired in 2021) as a major contributor to portfolio gains amid global demand for digital infrastructure tied to AI. Reuters similarly highlighted Blackstone’s data center expansion as a beneficiary of AI-driven demand.

This matters because data centers sit at the intersection of multiple Blackstone strengths:

- Scale deployment: data center platforms can absorb very large checks across land, power, construction, and long-term contracted assets.

- Perpetual capital compatibility: stable-yielding infrastructure fits products designed for long-duration capital.

- Credit adjacency: AI buildouts require financing—private credit can participate via loans and structured solutions.

Business Insider noted Blackstone’s infrastructure platform growth and pointed to private credit expansion tied to AI infrastructure needs. Even if you strip out the market’s hype cycle around AI software, the physical buildout—power, cooling, connectivity, and real assets—requires capital at a scale that few firms can consistently supply. Blackstone is clearly positioning itself as one of those firms.

Real estate: stabilization signals and BREIT’s rebound

Real estate has been the most scrutinized segment for large alternatives managers since rates rose and cap rates repriced. In that context, Blackstone’s update carried a confidence signal: the pressure points are stabilizing and performance is improving where the firm has differentiated exposure.

Barron’s highlighted a rebound across private equity and real estate and pointed to BREIT’s 8.1% return as evidence that parts of private real estate are recovering. Reuters likewise noted the BREIT rebound alongside the quarter’s broader strength.

That doesn’t mean “all clear.” The real estate market remains segmented—trophy logistics and data-center-adjacent assets are not the same as legacy office. But the results suggest that Blackstone’s ability to lean into secular demand (logistics, rental housing where appropriate, digital infrastructure-related real estate) is helping offset the areas still digesting higher financing costs.

Private credit: durable carry, disciplined underwriting, and the “institutional replacement” of banks

Private credit has become both a growth engine and a focal point for investor anxiety. On the one hand, credit’s carry profile is attractive; on the other, markets worry about late-cycle defaults, refinancing stress, and valuation opacity.

Blackstone’s results positioned credit as a steady performer inside the platform. Barron’s noted that private credit was “fine,” with reported gross returns exceeding 13% (in the context of broader segment strength) and emphasized the firm’s record fundraising year. Business Insider also framed private credit growth as linked to AI infrastructure and related buildouts.

The strategic logic is straightforward: as banks remain constrained—by regulation, capital charges, and risk appetite—private lenders have stepped in to finance large corporate needs, asset-backed structures, and infrastructure projects. For Blackstone, the opportunity isn’t only the yields; it’s the ability to deliver integrated capital solutions across equity and credit, increasing relevance with sponsors and corporates.

Shareholder returns: a large dividend and a reminder of the Blackstone “cash engine”

Blackstone’s shareholder model is still distinct: the firm returns significant cash via dividends tied to distributable earnings. The announced $1.49 per share dividend payable in February is a reminder that, even as the firm invests heavily for growth, it remains a cash-generating platform.

At the same time, the market’s immediate response underscored a recurring reality for alternatives stocks: investors can applaud results and still worry about forward risks. Reuters reported that despite beating expectations, Blackstone shares fell more than 3% in early trading, after initially rising premarket. That kind of reaction reflects how quickly sentiment can pivot toward concerns—private credit stress narratives, macro uncertainty, and policy risks—regardless of quarter-to-quarter execution.

The bigger picture: why Blackstone’s 2025 results matter for the entire alternatives industry

Blackstone’s Q4 and full-year report is more than a company update; it is a referendum on where institutional capital wants to concentrate in 2026.

Three implications stand out:

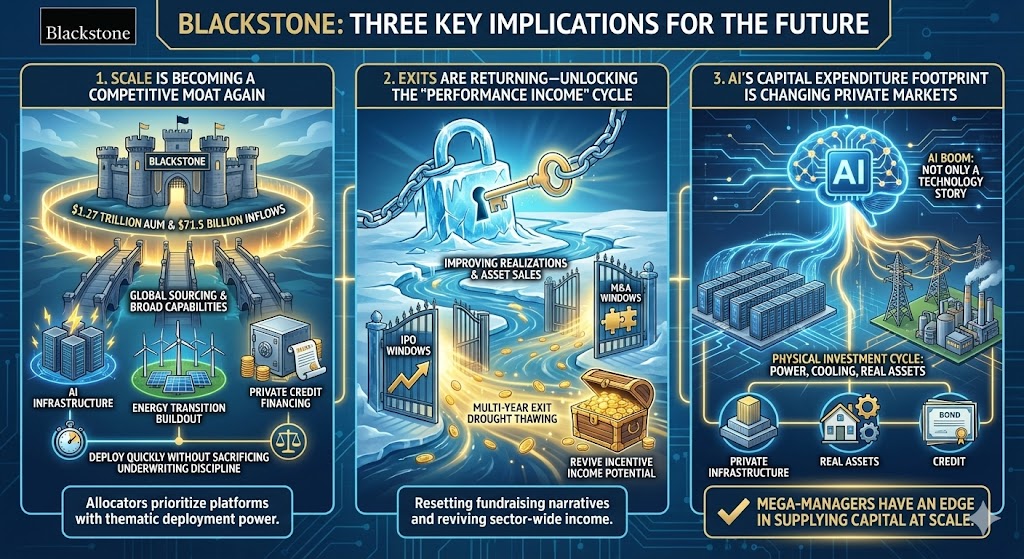

1) Scale is becoming a competitive moat again.

The combination of $71.5 billion quarterly inflows and $1.27 trillion AUM signals that allocators continue to prioritize platforms with broad capabilities and global sourcing. In the next cycle, the winners may be those who can deploy quickly into thematic opportunities—AI infrastructure, energy transition buildouts, and private credit financing—without sacrificing underwriting discipline.

2) Exits are returning—and that may unlock the “performance income” cycle.

Improving realizations and asset sales suggest that the multi-year exit drought is thawing. If IPO and M&A windows widen, it can reset fundraising narratives and revive incentive income potential across the sector.

3) AI’s capital expenditure footprint is changing private markets.

Blackstone’s data center and infrastructure posture shows that the AI boom is not only a technology story—it’s a physical investment cycle. That plays directly into private infrastructure, real assets, and credit—areas where mega-managers have an edge.

What to watch next

Going forward, investors will likely focus on a handful of indicators:

- Sustained fundraising pace (especially in perpetual and private wealth channels)

- Realization runway and the cadence of monetizations in private equity and real estate

- Credit performance as refinancing waves hit 2026–2027 maturities

- Infrastructure monetization—whether data center value creation can translate into realizations without sacrificing long-term compounding

Blackstone’s Q4 results don’t eliminate the risks in private markets, but they do reassert a powerful point: when capital cycles turn, the largest alternative platforms can accelerate quickly—capturing inflows, deploying at scale, and converting structural themes like AI infrastructure into durable fee streams.