(HedgeCo.Net) In early 2026, the most important trend at the largest U.S. hedge funds isn’t a single trade or a single market call. It’s the platform effect — the ability to generate steady returns across many teams, instruments, and time horizons while controlling risk tightly enough to survive violent cross-asset moves.

That story showed up clearly in January performance updates across major multi-manager complexes. A wide range of large funds posted gains to start the year, reinforcing the message allocators have been leaning into since 2024: in an uncertain macro environment, repeatable process beats heroic prediction.

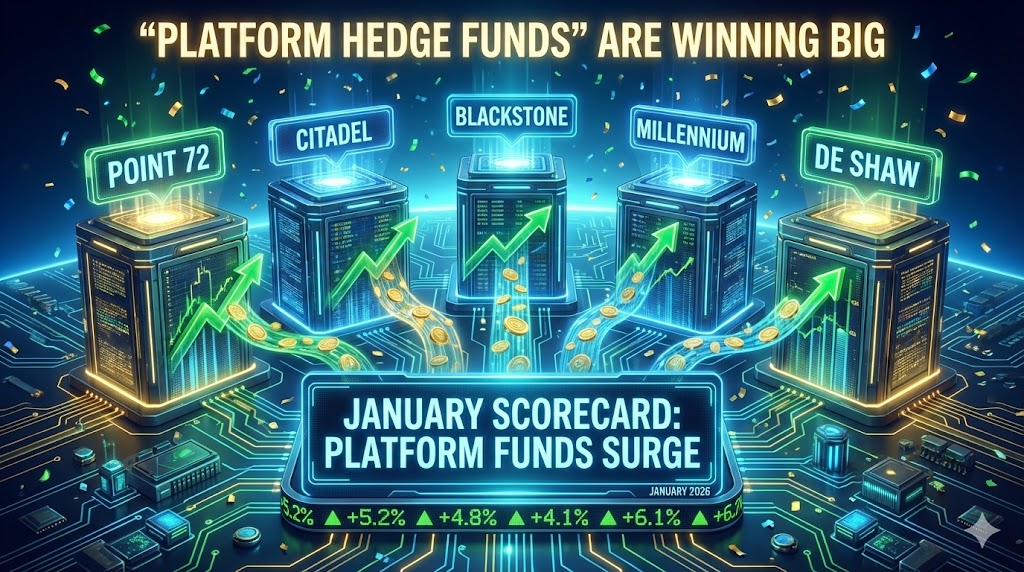

The “January tell”: steady gains across the biggest franchises

January performance data across major funds showed broadly positive starts, with names like Point72 Asset Management, Citadel, and several other multi-strats in the green.

The key here isn’t whether a flagship fund was up 1% or 3%. The key is what it implies about structure:

- The largest “pod shop” and multi-strategy platforms are built to extract return from many small edges.

- They’re designed for rapid re-risking when correlations break — and quick de-risking when conditions worsen.

- They monetize dispersion: the more markets and stocks behave differently, the more opportunity exists for relative-value, equity L/S, tactical macro, and stat-arb teams.

In January’s early read, that “stack of edges” approach looked like it worked — again.

Why “platform alpha” matters more in 2026 than it did five years ago

A large hedge fund in 2016 could still win with a few great PMs and an internal risk framework. In 2026, that’s rarely enough. The environment has become far less forgiving:

- Policy and geopolitical whiplash

Trade tension and shifting political priorities are pushing faster, sharper moves across FX, rates, and equities. That type of regime tends to punish slower-moving discretionary risk and reward firms with tight controls and rapid iteration. - Crowding is the default

Because information diffuses instantly, the industry’s consensus trades get crowded quickly. When positions are crowded, the unwind is brutal. In those moments, platforms tend to have the best survival trait: they can cut risk quickly, reallocate to other teams, and keep the machine running. - Talent depth is becoming a competitive moat

The largest funds are not just “funds” anymore. They operate like scaled financial enterprises: deep recruiting pipelines, training programs, internal mobility, and institutionalized non-investment infrastructure.

That “institutionalization” is visible in how mega funds are increasingly shaped by leadership roles outside pure investing. For example, leadership transitions in technology have been viewed as strategically meaningful at the very top tier.

What investors are actually demanding: quant + macro at the top of the wish list

Investor appetite is increasingly shaped by what worked in the last volatility cycle. Recent allocator surveys and prime brokerage commentary emphasize that quantitative and discretionary macro strategies are among the most desired exposures entering 2026.

This doesn’t mean everyone wants “a quant fund.” It means allocators want repeatability and robustness:

- Quant funds tend to scale process and diversify across signals.

- Discretionary macro, when done well, can monetize geopolitical and policy shocks.

- Both can provide return streams that look different from plain equity beta — a bigger deal when public markets are unstable.

In short: allocators want convexity, not just “stock picking.”

How the biggest U.S. funds are positioning for 2026: three themes

1) More emphasis on tactical trading units

Several large platforms have continued building out specialist units that can respond to event shocks and short-duration volatility — a hallmark of platform design. This shows up in the way certain fund segments outperform within larger complexes.

2) Expanding the “non-PM” backbone

As mega funds grow, the “enterprise layer” grows faster: risk, compliance, data engineering, security, execution, and operations. That reflects a core truth: you can’t run a $50B–$100B+ trading organization the way you ran a $5B one.

The scale trend is visible across major platforms, including examples like Millennium Management, where non-investment roles and organizational changes have become part of the story as much as performance.

3) Sharper differentiation between “good crowding” and “bad crowding”

Crowding is not automatically negative. “Good crowding” is when a firm has liquidity, risk controls, and exits mapped. “Bad crowding” is when leverage, illiquidity, and consensus combine. Platform funds are trying to keep exposures in the former bucket.

What this means for the rest of the hedge fund industry

When the biggest funds start the year strong, it creates a gravitational pull:

- Capital flows tend to concentrate in the platforms with the most stable track records.

- Talent flows follow, because top PMs increasingly want the resources and risk systems of the largest franchises.

- Smaller funds face a harsher bar: they must be meaningfully different, not just “smaller versions” of the big shops.

The market is effectively saying: “Show me your edge, or show me your scale.”

And January’s early performance snapshot — paired with allocator preference trends — suggests the largest U.S. funds are entering 2026 with exactly the kind of structure investors are paying for.