Structural Diversification in an Era of Correlated Volatility:

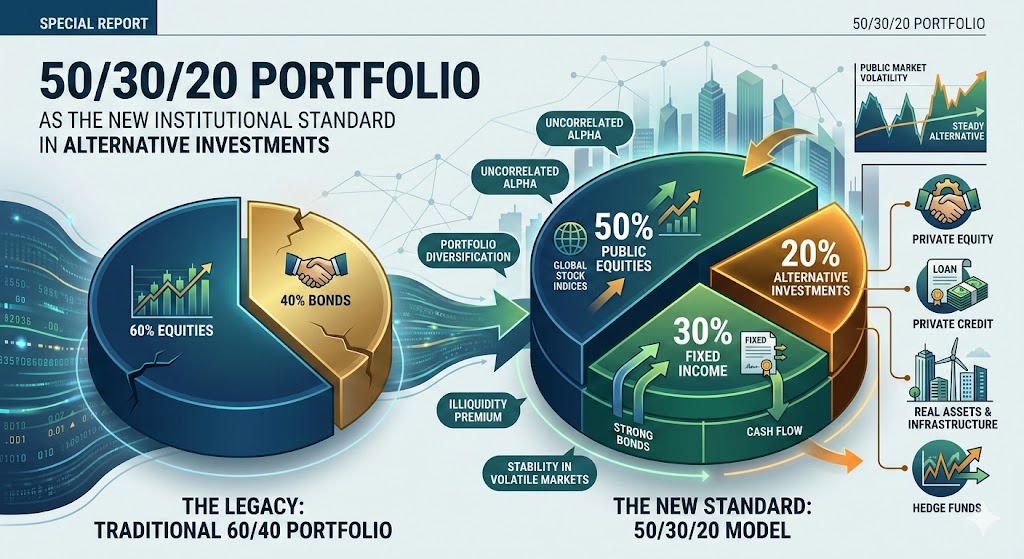

(HedgeCo.Net) The 60/40 portfolio—the bedrock of modern portfolio theory—was officially declared dead in the “Inflationary Shock” of 2022. By 2026, its successor has been codified: the 50/30/20 Portfolio (50% Public Equities, 30% Fixed Income, 20% Private Alternatives). This shift represents more than just a change in percentages; it is a fundamental rejection of the idea that public markets alone can provide sufficient diversification.

The Shrinking Public Universe

The math driving the 50/30/20 shift is undeniable. In 1996, there were over 7,000 public companies in the U.S.; today, that number has dwindled to roughly 3,700. Companies are staying private longer, fueled by venture capital and late-stage private equity. By the time a company like a “SpaceX” or a “ByteDance” goes public, the “hyper-growth” phase has already been captured by private investors. For a retail investor, a 100% public portfolio is, by definition, missing out on the most innovative sectors of the global economy.

The “Alpha” vs. “Beta” Distinction

In the 50/30/20 model, the 20% “Alternatives” bucket is designed to solve two distinct problems:

- The Beta Problem: Public stocks (the 50%) are increasingly dominated by a handful of tech giants. When the “Magnificent Seven” (or their 2026 equivalents) sneeze, the entire index catches a cold. Alternatives provide “uncorrelated beta”—returns driven by factors like real estate cycles or infrastructure demand.

- The Alpha Problem: With high-frequency trading and AI-driven arbitrage, public markets are “hyper-efficient.” Finding an “edge” is nearly impossible. Private markets, being opaque and relationship-driven, still offer “complexity premiums” and “illiquidity premiums.”

The “Retailization” Engine

The 20% target would be impossible without the massive technological overhaul of the wealth management industry. Platforms like iCapital and CAIS have effectively “Uber-ized” the subscription process. A financial advisor in a mid-sized firm can now move a client into a blue-chip PE fund with the same ease as buying an ETF. This “democratization” has unlocked a massive pool of “dry powder”—estimated at over $4 trillion in untapped HNW capital—that is now flooding into the alts space.